Drained retirement savings

24 January 2021, 1:30 AM

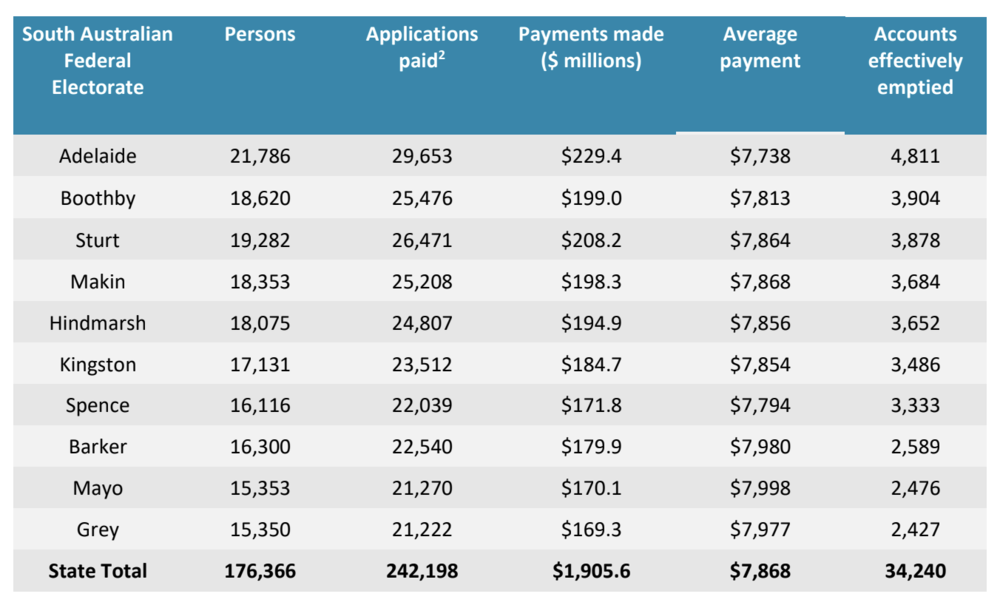

More than 34,000 South Australians have effectively wiped out their super savings as the state’s workers have withdrawn nearly $2 billion from their retirement nest eggs, sparking fears that if the legislated super rate increase is dumped more workers will retire with less and be more reliant on the aged pension.

New Industry Super Australia analysis estimates South Australians have made more than 240,000 applications via the early release of super scheme, withdrawing on average $7,868 per application.

The top three federal electorates by withdrawals were Adelaide $229 million, Sturt $208 million and Boothby $199 million.

In April the government broke open super’s preservation rules allowing Australians who had lost their jobs or had hours reduced to access $10,000 in super before July 1 and a further $10,000 until December.

But accessing super early comes at a steep price to their savings, a 30-year-old who withdraws $20,000 could have up to $80,000 less at retirement.

There is also a cost to the public purse, as for every $1 taken out by someone in their 30s the taxpayer contributes up to $2.50 in increased pension costs.

Only the super guarantee increase can save future generations of taxpayers from the massive extra pension cost of the early release and help young Australians retirement savings recover.

Ditching the legislated increase would heap pressure on the pension and be a cruel blow to the Victorians who had to make the tough choice to sacrifice retirement savings to get them through the pandemic.

Proposals to make the increase optional would see the government reap billions in higher taxes, it would slug a couple, each on average earnings, with a $20,000 higher tax bill.

ISA analysis shows that if the super rate increase were cut, an average 30-year-old man who took $20,000 from their super would either lose $180,000 from their retirement or be forced to work until 74, while an average 30-year-old female would need to work an extra eight years or have $150,000 less at retirement.

The government’s Retirement Income Review did not model the impacts to the Federal Budget or the retirement adequacy impacts of the 3 million Australians withdrawing super early. But it cautioned against early release-style schemes because they lead to a significant decrease in young people’s savings.

The super rate is legislated to rise from 9.5% to 12% by 2025 – with the first small 0.5% increase in July. Comments attributable to Industry Super Australia deputy Chief Executive Matthew Linden:

“The South Australians who had to make the tough call to access their super did so with the confidence that the government has promised to give them a super boost.”

“Ripping it away from them would be a cruel double blow, it would leave them with far less at retirement and saddle the next generation with a whopping pension.”

“Super is not a cookie jar for government to raid to solve short-term Budget problems, nor for housing or to solve stagnant wage growth. Dipping into super early comes at a steep cost for the individual and the future taxpayers, as a society we shouldn’t be demanding our young people pay the price again.”

Table 1: SA electorates accessing early release, ranked by number of people wiping out their balance

1 The estimates are based on ISA analysis of the impacts of COVID-19 on electorate employment using ABS payroll data by industry, gender and age. The estimates use Treasury statistics on the state, gender and age distribution of early release and are benchmarked to the latest APRA early release data up to 20 December 2020, published on 6 January 2021. Estimates of the number of accounts that have been wiped out are based on ATO data on the distribution of superannuation balances by region, gender and age.

2 There is a lag between the applications being made and the reporting of payments being made. Very few applications are rejected.